South Africa’s automotive market delivered a powerful performance in March 2026, with new vehicle sales climbing to their highest level for the month in almost two decades. The figures reflect a sector still benefiting from improved domestic conditions, even as warning signs begin to emerge in the broader economic landscape.

Data from naamsa shows that the market’s strength is being driven primarily by local demand. Earlier interest rate cuts, easing inflation at the start of the year, and a steady improvement in confidence have combined to support vehicle purchases across key segments. However, the external environment is shifting rapidly, introducing new pressures that could test this momentum in the months ahead.

Retail demand remains the backbone

A defining feature of the current upswing is the dominance of dealer driven sales. The bulk of vehicles sold in March went through retail channels, highlighting the central role of private consumers and smaller businesses in sustaining the recovery.

This points to a market that is not reliant on large scale fleet or government orders, but rather on underlying consumer activity. While this is a positive signal of organic demand, it also makes the market more sensitive to changes in household finances and borrowing costs.

Passenger vehicles led the growth, reflecting renewed consumer confidence and improved affordability earlier in the year. Lower interest rates have played a key role here, reducing monthly repayments and making vehicle ownership more accessible.

Commercial segments show steady gains

Beyond passenger cars, the light commercial vehicle segment also recorded solid growth. Demand in this category is typically linked to small business activity, logistics, and trade, suggesting that parts of the economy are seeing gradual improvement.

Medium and heavy commercial vehicles posted more moderate increases, but their performance remains significant. These segments are closely tied to infrastructure investment, freight demand, and broader industrial activity. Their expansion indicates that business confidence is translating into real spending, even if at a measured pace.

At the same time, these categories remain highly exposed to shifts in economic conditions, particularly fuel costs and electricity reliability, both of which continue to influence operating expenses.

Exports under strain

While the domestic market continues to perform well, exports are facing ongoing pressure. Vehicle shipments declined in March, reflecting a more challenging global environment.

Geopolitical tensions and weaker demand in key international markets are weighing on export performance. This creates a growing imbalance in the industry, where local sales are offsetting weaker external demand. Over time, this could place pressure on production volumes and investment decisions.

Policy support and industry direction

The release of the March sales data coincides with renewed emphasis on investment led growth following the South Africa Investment Conference. Government policy continues to position the automotive sector as a key pillar of industrial development.

There is increasing focus on localisation, infrastructure expansion, and long term competitiveness. At the same time, the shift towards new energy vehicles is gaining prominence. Electric vehicle production and battery technologies are being framed as strategic opportunities, rather than simply regulatory requirements.

This transition could strengthen South Africa’s role in global value chains, particularly given its access to critical minerals. However, success will depend on consistent policy implementation and improvements in logistics and energy supply.

Rising costs cloud the outlook

Despite the strong March showing, the macroeconomic backdrop is becoming less supportive. Inflation, which had eased earlier in the year, is now under renewed pressure due to higher global oil prices.

The resulting fuel price increases are expected to raise transport and operating costs across the economy. While temporary tax relief provides some support, it does not fully offset the impact, meaning consumers and businesses are likely to feel the strain.

Consumer confidence has improved, but the recovery remains uneven. Higher income households have seen the greatest benefit, while lower income groups continue to face financial pressure. This limits the depth of demand and raises concerns about sustainability.

Business confidence, by contrast, has strengthened more broadly, with vehicle dealers in particular reporting high levels of optimism. This aligns with the recent sales performance, but may come under pressure if costs continue to rise.

The South African Reserve Bank’s decision to hold interest rates steady reflects this uncertain environment. After a period of easing, policymakers are now taking a more cautious stance as inflation risks re emerge.

Key figures

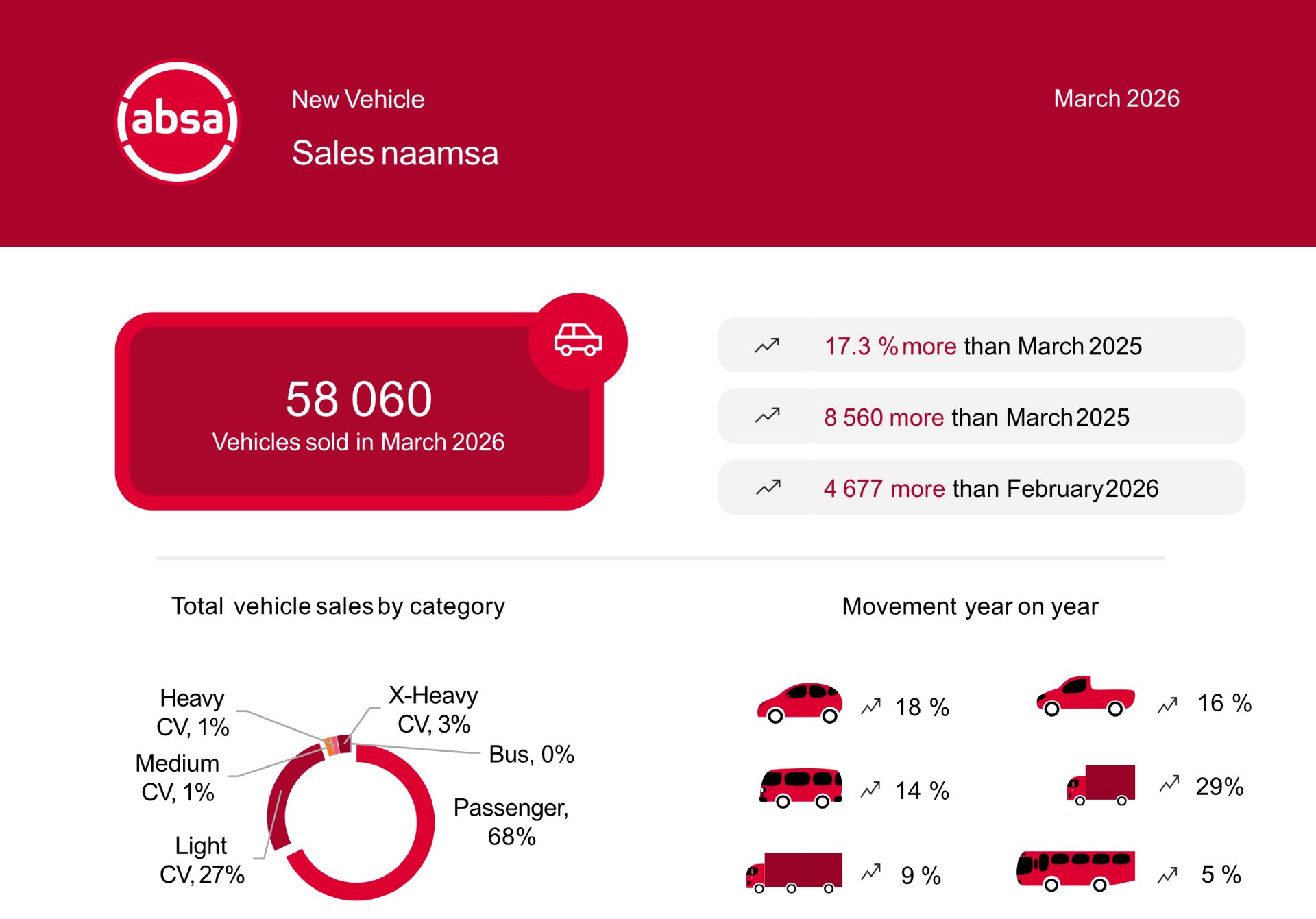

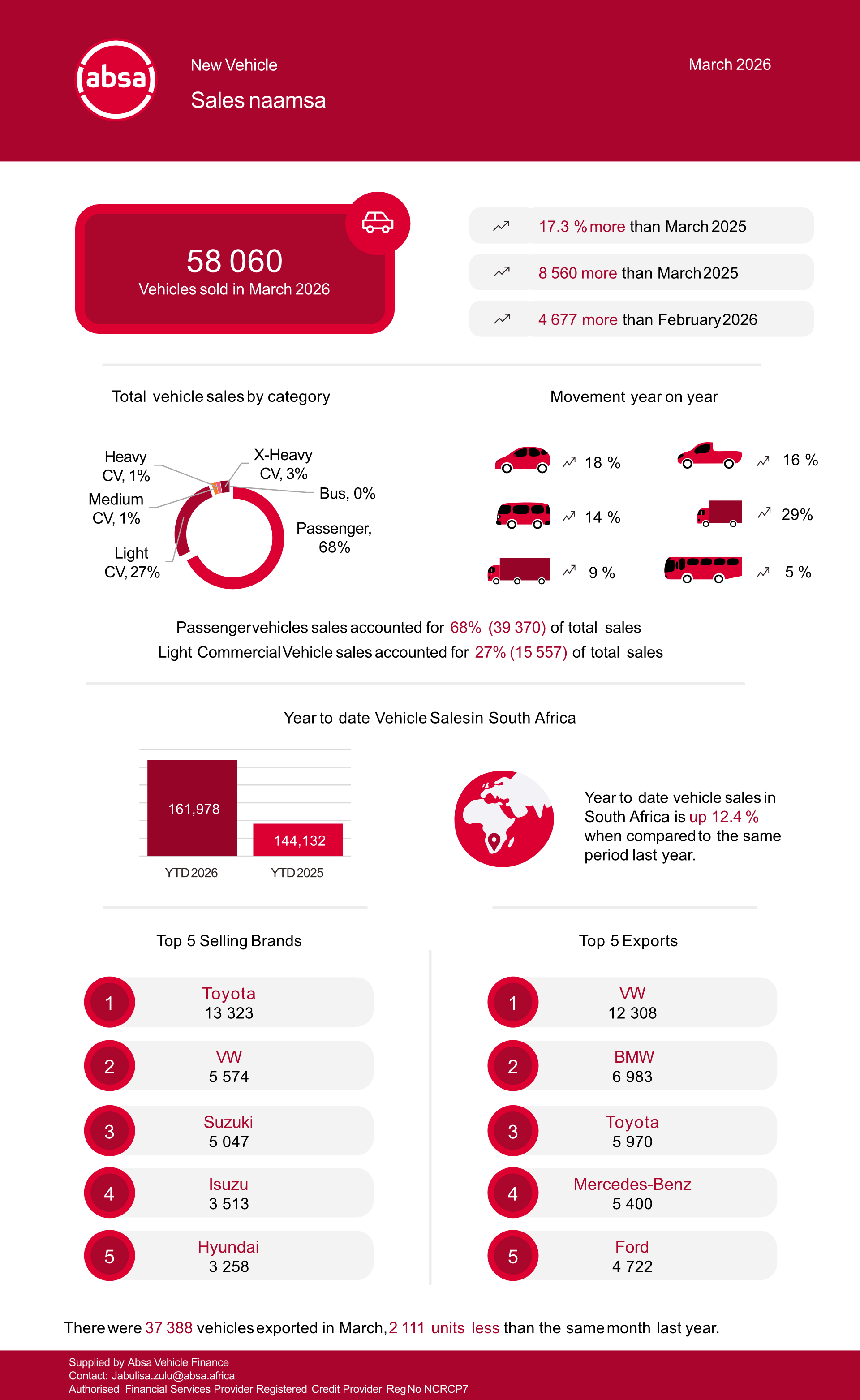

March 2026 sales reached 58060 units, up 17.3% year on year. Passenger vehicles totalled 39370 units and light commercial vehicles 15557 units. Medium commercial vehicles recorded 823 units and heavy trucks and buses 2310 units. Exports fell to 37388 units, down 5.3%.